Fintech apps: 4 themes & 9 trends to watch in 2024

Are fintech apps still hot? According to a recent report by Boston Consulting Group, the answer is pretty much “yes, but …”

The bad news is that fintech funding has plummeted 71% since the pandemic. The good news is that revenue growth has increased every year since 2021 and is now at a 14% compound annual growth rate. The even better news: fintech has a projected market size of $1.5 trillion in revenue by 2030.

That’s a staggering 5X growth from today and it means that there’s a ton of potential for fintech apps in 2024 and beyond.

Let’s dig in.

First, the big numbers for fintech and fintech apps

Fintech is not a small space. Literally everyone has to deal with money, and for most of us, that means banking and fintech apps. Mobile apps are where the growth is: global fintech revenue keeps growing, and the percentage captured by challenger banks that tend to be more digitally savvy also keeps growing.

Here’s the big fintech picture:

- $1.5 trillion

Global fintech revenue by 2030 - 14% growth

Annual global fintech revenue growth - $320 billion

Embedded finance revenue by 2030 - 100 million customers

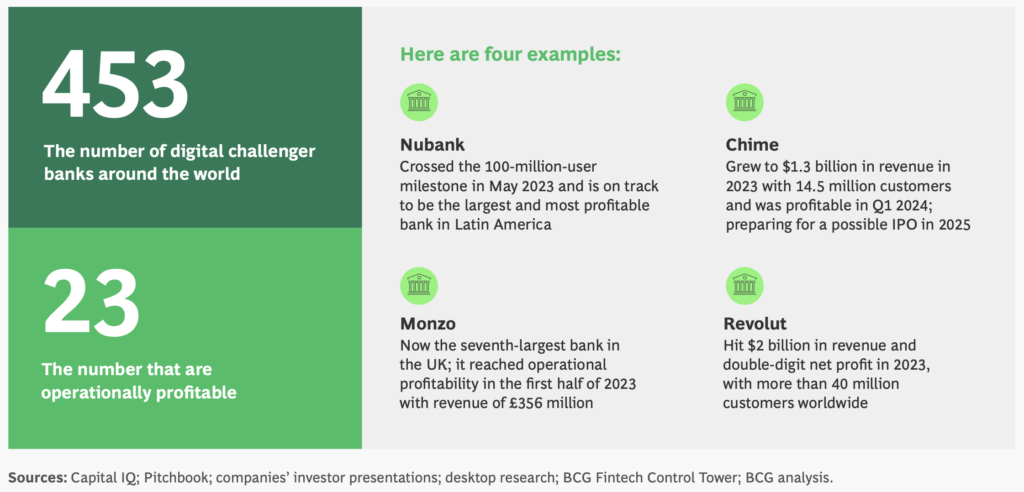

Neobanks are getting bigger: Brazil’s Nubank just crossed this customer threshold - 453 challenger banks

The number of neobanks across the world as of 2024 - 71% funding drop

$42 billion investment in 2023 versus $114 billion in 2021

Add it all up, and while fintech apps have a bright future, they’ll need to get there more efficiently on less capital and with a greater focus on profitable growth, not just growth at all costs.

4 major fintech themes right now

Fintech took off with cheap money and restricted travel during the pandemic. But while its wings might be a bit clipped now, big trends continue to shape fintech and fintech apps.

1. Embedded finance

Embedded finance is the integration of financial services into non-financial platforms or products. The result is a hybrid that offers multiple services in a single place.

A few examples:

- Lyft or Uber embedding a wallet into their apps

- Amazon offering point-of-sale financing

- Walmart operating as a banking service with checking and savings accounts

- Expedia offering insurance along with your trip

- Apple and Google offering payment technology as well as a wallet

Embedded finance will be a $320 billion market by 2030, says BCG. Half of that will be SMBs, $120 billion will be consumer offerings, and another $50 billion will be in the enterprise segment, according to their projections.

2. Connected commerce

Connected commerce is an integration of financial services into diverse digital ecosystems, including the adtech space.

Banks are custodians of some of the most insightful data about their customers, BCG says, and that provides opportunities to target ads much more effectively than many other existing adtech players.

“With the increasing value of first-party data, given cookie depreciation and app-tracking transparency, connected commerce is emerging as a triple play for banks—it creates a new revenue stream, increases customer loyalty, and enables banks to offer a marketing channel to their SMB and enterprise customers,” BCG says.

Examples of early contenders:

- Chase Media Solutions in the adtech space

- CapitalOne Shopping in the deals/coupons space

- Citi Shop in the loyalty space

- PayPal’s new advertising service

- Revolut is “exploring plans to monetise customer data through sharing it with advertising partners” according to the Financial Times

It’s unclear both how big connected commerce can get in fintech, and also how customers will react to their second-most-sensitive data being shared with advertisers (medical data is even more sensitive than financial).

Clearly, they’ll need some kind of assurance of identity anonymization, at minimum, if their data is being shared. Doing it wrong could kill a neobank or seriously damage a traditional financial institution’s brand image.

3. Open banking

Open banking involves third-party services connecting to your bank to provide additional services. In open banking, third-party developers build applications using financial data that customers permit their bank to share.

Budgeting and investment applications come to mind when you think of open banking, but it’s still largely a nascent space driven by regulation. 65 countries have enacted some form of open banking legislation, including:

- The EU’s Revised Payment Services Directive (PSD2)

- UK’s Open Banking initiative

- Australia’s Consumer Data Right (CDR) framework

That said, there hasn’t been a lot of uptake. Only 12% of people in the EU have taken advantage of open banking services and products, and it’s lower than 30% in Sweden and Norway, early advocates for open banking. That’s not a shock: while we might be OK using our Google or Apple or social identities for logging in all around the internet, it’s hard to convince us to connect our bank accounts to a random app or website.

Where’s the big opportunity for fintech apps and open banking?

Potentially in adtech, according to BCG:

“We believe that open banking will continue to be relevant but is unlikely to change the basis of competition in consumer banking … in advertising, access to transaction-level data will enable more timely and targeted personal offers.”

The same kinds of privacy concerns apply as in connected commerce, of course.

4. Generative AI

I just used ChatGPT 4o to summarize about 30 pages of investment statements down to a few paragraphs and bullet points. Generative AI will be big in fintech, but not for product innovation, says BCG.

Instead, it’ll be focused on productivity enhancements.

“GenAI is already delivering tangible productivity gains in financial services … the use of GenAI in product innovation will lag its uses for productivity—but we expect it to follow.”

9 trends in fintech and fintech apps

Those 4 themes intersect somewhat with 9 existing and emerging trends in fintech, BCG says. They include:

- High interest rates

- Convergence of evolving regulations around finance, fintech apps, and fintech-adjacent areas like crypto

- New regulations around KYC and AML

- Acceleration of digital public infrastructure: digital governance

- Fraud and cybersecurity

- Generative AI

- Embedding financial services into more and more apps

- Alliances between fintech and adtech

- IPO and M&A markets re-emerging over the next few years

Fintech apps and growth

What does this mean for banks, neobanks, and fintech apps?

In short, it means get busy getting profitable.

The cash-flooded days of over $100 billion of fintech investment in 2021 are gone. The ability to access non-dilutive capital for debt financing is also largely gone, thanks to higher interest rates. That means it’s absolutely critical to use your remaining capital efficiently and to grow profitably, not wildly.

And growth is still possible.

There are still billions of unbanked people across the globe, highlighting the ongoing opportunity. With fintech revenues growing by 14% annually over the past 2 years, there’s an opportunity to continue growing while making money.

In addition, fintech apps and brands are expanding their addressable market space by providing wallets, financing, insurance, and even investment embedded into non-traditional contexts.

Although neobanks speak technology like a native, traditional banks have an advantage, according to the BCG report. Banks get 55% more usage per month than fintech apps, and 78% of their customers open banking apps weekly. That opens the door for traditional banks to offer what the neobanks and fintech apps have promised for years.

Stay up to date on the latest happenings in digital marketing